UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the Fiscal Year Ended December 31, 2016 Commission File Number: 0‑3676

VSE CORPORATION

(Exact Name of Registrant as Specified in its Charter)

|

| |

DELAWARE | 54-0649263 |

(State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) |

|

| | | | |

6348 Walker Lane | | | | |

Alexandria, Virginia | | 22310 | | www.vsecorp.com |

(Address of Principal Executive Offices) | | (Zip Code) | | (Webpage) |

Registrant's Telephone Number, Including Area Code: (703) 960-4600

Securities registered pursuant to Section 12(b) of the Act:

|

| |

Title of each class | Name of each exchange on which registered |

Common Stock, par value $.05 per share | The NASDAQ Global Select Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ ] No

[x]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes [ ] No [x]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [x] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes [x] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer [ ] Accelerated filer [x] Non-accelerated filer [ ] Smaller reporting company [ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes [ ] No [x]

The aggregate market value of outstanding voting stock held by non-affiliates of the Registrant as of June 30, 2016, was approximately $284 million based on the last reported sales price of the registrant's common stock on The NASDAQ Global Select Market as of that date.

Number of shares of Common Stock outstanding as of February 27, 2017: 10,814,927.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of Registrant's definitive proxy statement for the Annual Meeting of Stockholders expected to be held on May 2, 2017, are incorporated herein by reference into Part III of this report.

|

| | |

TABLE OF CONTENTS |

| | Page |

| | |

| | |

ITEM 1 | | |

ITEM 1A | | |

ITEM 1B | | |

ITEM 2 | | |

ITEM 3 | | |

ITEM 4 | | |

ITEM 4(a) | | |

| | |

| | |

| | |

ITEM 5 | | |

ITEM 6 | | |

ITEM 7 | | |

ITEM 7A | | |

ITEM 8 | | |

ITEM 9 | | |

ITEM 9A | | |

ITEM 9B | | |

| | |

| | |

| | |

ITEM 10 | | |

ITEM 11 | | |

ITEM 12 | | |

ITEM 13 | | |

ITEM 14 | | |

| | |

| | |

| | |

ITEM 15 | | |

| | |

| | |

| | |

| | |

Forward Looking Statements

This Annual Report on Form 10-K ("Form 10-K") contains statements that, to the extent they are not recitations of historical fact, constitute "forward looking statements" under federal securities laws. All such statements are intended to be subject to the safe harbor protection provided by applicable securities laws. For discussions identifying some important factors that could cause actual VSE Corporation ("VSE," the "Company," "us," "our," or "we") results to differ materially from those anticipated in the forward looking statements contained in this filing, see VSE's "Narrative Description of Business" (Items 1, 1A, 2 and 3), and Item 7 "Management's Discussion and Analysis of Financial Condition and Results of Operations." Readers are cautioned not to place undue reliance on these forward looking statements, which reflect management's analysis only as of the date hereof. The Company undertakes no obligation to publicly revise these forward looking statements to reflect events or circumstances that occur or arise after the date hereof. Readers should also carefully review the risk factors described in other documents the Company files from time to time with the Securities and Exchange Commission, including Quarterly Reports on Form 10-Q filed by the Company subsequent to this Form 10-K and any Current Reports on Form 8-K filed by the Company.

PART I

ITEM 1. Business

(a) General Background

We are a diversified services and supply chain management company that assists our clients in sustaining, extending the service life, and improving the performance of their transportation, equipment, and other assets and systems. We provide logistics and distribution services for legacy systems and equipment and professional and technical services to the United States Government (the "government"), including the United States Department of Defense ("DoD"), the United States Postal Service ("USPS"), federal civilian agencies, and commercial and other customers. Our largest customers are the DoD and the USPS. Our operations include supply chain management solutions, parts supply and distribution, and maintenance, repair, and overhaul (“MRO”) services for vehicle fleet, aviation, and other clients; vehicle and equipment maintenance and refurbishment; logistics; engineering; energy and environmental services; IT and health care IT solutions; and consulting services.

VSE was incorporated in Delaware in 1959 and the parent company serves as a centralized managing and consolidating entity for our operating groups, each of which consists of one or more subsidiaries (all of which are wholly owned) or unincorporated divisions that perform our services. VSE’s operating groups include our Supply Chain Management Group, Aviation Group, Federal Services Group, and IT, Energy and Management Consulting Group. The term "VSE" or "Company" means VSE and its subsidiaries and divisions unless the context indicates operations of only VSE as the parent company.

(b) Financial Information

Our operations are conducted within four reportable segments aligned with our operating groups: (1) Supply Chain Management, which generated 29.7% of our revenues in 2016; (2) Aviation, which generated 19.3% of our revenues in 2016; (3) Federal Services, which generated approximately 44.2% of our revenues in 2016; and (4) IT, Energy and Management Consulting, which generated 6.8% of our revenues in 2016. Additional financial information for our reportable segments appears in Item 7 "Management’s Discussion and Analysis of Financial Condition and Results of Operations” and in Item 8 "Financial Statements and Supplementary Data” of this Form 10-K.

(c) Description of Business

Services and Products

We apply a broad array of capabilities and resources to support our clients’ transportation assets, vehicle fleets, aircraft, systems, equipment and processes. We focus on creating value by sustaining the life and improving the performance of our client assets through core offerings in supply chain management, MRO, equipment refurbishment, logistics and engineering. We also provide IT solutions, health care IT, and consulting services.

Typical service offerings include supply chain and inventory management services; vehicle fleet sustainment programs; vehicle fleet parts supply and distribution; MRO of aircraft engines and engine components; aircraft engine parts supply and distribution; engineering support for military vehicles; military equipment refurbishment and modification; ship MRO and follow-on technical support; logistics management support; machinery condition analysis; specification preparation for ship alterations; ship’s force crew training; life cycle support for ships; ship communication systems; energy conservation, energy efficiency, sustainable energy supply, and electric power grid modernization projects; technology road-mapping; IT enterprise architecture development, information assurance/business continuity, security risk management, and network services; medical logistics; and medical command and control. See Item 7 “Management’s Discussion and Analysis of Financial Information and Results of Operations” below for more information regarding our business.

Revenues and Contracts

Our revenues are derived from the delivery of products and from contract services performed for our clients. We offer our products and professional and technical services through various ordering agreements and negotiated and competitive contract arrangements.

Our Supply Chain Management Group revenues result from the sale of vehicle parts to the USPS and other government and commercial clients. We recognize revenue from the sale of vehicle parts when the customer takes ownership of the parts.

Our Aviation Group revenues result from the sale of aircraft parts and performance of MRO services for private and commercial aircraft owners, other aviation MRO providers, and aviation original equipment manufacturers. We recognize revenues upon the shipment or delivery of products to customers based on when title or risk of loss transfers to the customer.

Our Federal Services and IT, Energy and Management Consulting Group revenues result primarily from cost plus fixed fee, cost plus award fee, time and materials, or fixed-price contracts with the government. Revenues result from work performed on these contracts by our own employees, from work performed by our subcontractors, and from costs of materials used in performing the work. Revenues on cost‑type contracts are recorded as allowable costs are incurred and fees are earned. Revenues for time and materials contracts are recorded on the basis of allowable labor hours worked multiplied by the contract defined billing rates, plus the cost of materials used in performance on the contract. Profits or losses on time and material contracts result from the difference between the cost of services performed and the contract defined billing rates for these services. Revenue recognition methods on fixed-price contracts vary depending on the nature of the work and the contract terms. Revenues on fixed-price service contracts are recorded as work is performed, typically ratably over the service period. Revenues on fixed-price contracts that require delivery of specific items are recorded based on a price per unit as units are delivered.

The USPS, U.S. Army, and U.S. Navy are our largest customers. Our customers also include various other government and commercial entities.

|

| | | | | | | | | | | | | | | | | | | | | |

| | Revenues by Customer (dollars in thousands) Years ended December 31, |

Customer | | 2016 | | % | | 2015 | | % | | 2014 | | % |

U. S. Postal Service | | $ | 181,215 |

| | 26.2 |

| | $ | 184,876 |

| | 34.6 |

| | $ | 167,268 |

| | 39.4 |

|

| | | | | | | | | |

| | |

U.S. Navy | | 190,155 |

| | 27.5 |

| | 98,887 |

| | 18.5 |

| | 88,007 |

| | 20.7 |

|

U.S. Army | | 139,764 |

| | 20.2 |

| | 80,086 |

| | 15.0 |

| | 101,714 |

| | 24.0 |

|

U.S. Air Force | | 3,482 |

| | 0.5 |

| | 3,558 |

| | 0.7 |

| | 3,323 |

| | 0.8 |

|

Total - DoD | | 333,401 |

| | 48.2 |

| | 182,531 |

| | 34.2 |

| | 193,044 |

| | 45.5 |

|

| | | | | | | | | |

| | |

Commercial Aviation | | 131,067 |

| | 19.0 |

| | 119,729 |

| | 22.4 |

| | — |

| | — |

|

Other Commercial | | 10,721 |

| | 1.5 |

| | 4,653 |

| | 0.9 |

| | 3,680 |

| | 0.9 |

|

Total - Commercial | | 141,788 |

| | 20.5 |

| | 124,382 |

| | 23.3 |

| | 3,680 |

| | 0.9 |

|

| | | | | | | | | | | | |

Department of Energy | | 11,708 |

| | 1.7 |

| | 16,020 |

| | 3.0 |

| | 19,000 |

| | 4.5 |

|

Social Security Administration | | 9,762 |

| | 1.4 |

| | 9,666 |

| | 1.8 |

| | 10,153 |

| | 2.4 |

|

Other Government | | 13,916 |

| | 2.0 |

| | 16,507 |

| | 3.1 |

| | 30,926 |

| | 7.3 |

|

Total - Other Civilian Agencies | | 35,386 |

| | 5.1 |

| | 42,193 |

| | 7.9 |

| | 60,079 |

| | 14.2 |

|

| |

| | | | | | | |

| | |

Total | | $ | 691,790 |

| | 100.0 |

| | $ | 533,982 |

| | 100.0 |

| | $ | 424,071 |

| | 100.0 |

|

Backlog

Funded backlog represents a measure of potential future revenues from work performed by our Federal Services and IT, Energy and Management Consulting groups on government contracts. Funded backlog is defined by us as the total value of contracts that has been appropriated and funded by the procuring agencies, less the amount of revenues that have already been recognized on such contracts. Our reported backlog is comprised of funding received by us in incremental amounts for work that is generally expected to be completed within six to 12 months following the award of the funding. Our funded backlog for our Federal Services and IT, Energy and Management Consulting groups as of December 31, 2016, was approximately $322 million and as of December 31, 2015 and 2014 it was approximately $238 million and $193 million, respectively. Changes in funded backlog on contracts are sometimes unpredictable due to uncertainties associated with changing government program priorities and availability of funds, which is heavily dependent upon the congressional authorization and appropriation process. Delays in this process may temporarily diminish the availability of funds for ongoing and planned work.

In addition to funded backlog levels, we have contract ceiling amounts available for use on multiple award, indefinite delivery, indefinite quantity contracts with DoD and federal civilian agencies. While these contracts increase the opportunities

available for us to pursue future work, the actual amount of future work is indeterminate until task orders are placed on the contracts. Frequently, these task orders are competitively awarded. Additionally, these task orders must be funded by the procuring agencies before we can perform work and begin generating revenues.

Marketing

Our marketing activities are conducted at the operating group level by our marketing and business development staff and our professional staff of sales representatives, managers, and other personnel. New customer contacts and information concerning new programs, requirements and opportunities become available through attendance at industry trade shows and events, through sales calls and client servicing, through negotiation with key business partners, through formal and informal briefings, from participation in professional organizations, in the course of contract performance, and from literature published by government, trade associations, professional organizations and commercial entities.

Personnel

Our employees have a variety of specialized experience, training, and skills that provide the expertise required to service our clients. Some have high levels of education. As of December 31, 2016, we had 2,523 employees, an increase from 2,057 as of December 31, 2015. Principal employee categories include (a) mechanics and vehicle, aircraft, and equipment technicians, (b) logisticians, (c) warehouse and sales personnel, (d) engineers and technicians in mechanical, electronic, industrial, energy and environmental services, and (e) information technology professionals in computer systems, applications and products, configuration, change and data management disciplines. The expertise required by our customers frequently includes knowledge of government regulations and procedures.

We actively seek initiatives and participate in outreach programs to assist individuals who have served in the U.S. Armed Forces. These efforts include an emphasis on hiring military veterans, which we believe enhances the quality of our workforce. Approximately 30% of our employees have previously served as members in the U.S. Armed Forces.

Competition

The supply chain, logistics, and MRO services offered by our Supply Chain Management and Aviation groups and the federally contracted professional and technical services offered by our Federal Services and IT, Energy and Management Consulting groups are conducted in very competitive operating environments.

The vehicle parts aftermarket and aviation parts and servicing markets are fragmented, with many large and small competitors that compete for our customer base.

Large diversified federal contracting firms with greater financial resources and larger technical staffs are capable of providing the same services offered by us. Government agencies emphasize awarding contracts on a competitive basis as opposed to a sole source or other noncompetitive basis. Most of the significant contracts under which we currently perform services were either initially awarded on a competitive basis or have been renewed at least once on a competitive basis. There is no assurance regarding the level of work we may obtain under some of these contracts. Government budgets, and in particular the budgets of certain government agencies, can also affect competition in our business. A general decline in government budgets, a reallocation of government spending priorities, or a reallocation of work for small business set-aside programs that results in lower levels of potential business in the markets we serve or the services we offer will cause increased competition.

The extent of competition that we will encounter as a result of changing economic or competitive conditions, customer requirements or technological developments is unpredictable. We believe the principal competitive factors for our business are customer knowledge, technical and financial qualifications, past performance, government budgetary stress, and price, which has been more heavily weighted in recent years.

Available Information

Copies of our publicly available Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports are filed with or otherwise furnished to the Securities and Exchange Commission (“SEC”) pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended. Such reports and amendments are also available free of charge through our website www.vsecorp.com as soon as reasonably practicable after the reports are electronically filed with the SEC.

ITEM 1A. Risk Factors

Our future results may differ materially from past results and from those projected in the forward-looking statements contained in this Form 10-K due to various uncertainties and risks, including those risks set forth below, non-recurring events and other important factors disclosed previously and from time to time in our other reports filed with the SEC.

Uncertain government budgets and shifting government priorities could delay contract awards and funding and adversely affect our ability to continue work under our government contracts. Additionally, federal procurement directives could result in our loss of work on current programs to small business set-asides and large multiple award contracts.

Our government business is subject to funding delays, terminations (including at the government's convenience), reductions, in-sourcing, extensions, and moratoriums associated with the government’s budgeting and contracting process. The federal procurement environment is unpredictable and could adversely affect our ability to perform work under new and existing contracts. We have experienced delays in contract awards and funding on our contracts in recent years that have adversely affected our ability to continue existing work and to replace expiring work. Additionally, our government business is subject to the risk that one or more of our potential contracts or contract extensions may be diverted by the contracting agency to a small or disadvantaged or minority-owned business pursuant to set-aside programs administered by the Small Business Administration, or may be bundled into large multiple award contracts for very large businesses. These risks can potentially have an adverse effect on our revenue growth and profit margins.

Increased market competition resulting from decreases in government spending for contract services and government contracting award criteria could adversely affect our ability to sustain our revenue levels.

Pressure on government budgets may adversely affect the flow of work to federal contractors, particularly new programs. Competitor contractors that experience a loss of government work have tended to redirect their marketing efforts toward the types of work that we perform. This increase in competition for our service offerings has adversely affected our ability to win new work or successor contracts to continue work that is currently performed by us under expiring contracts. Unsuccessful bidders frequently protest contract awards, which can delay or reverse the contract awards. Additionally, the government has trended toward contract award criteria that emphasizes lowest price, technically acceptable bids, which further intensifies competition in our government markets.

Certain programs comprise a material portion of our revenue. Our work on large government programs presents a risk to revenue growth and profit margins and sustainability.

The eventual expiration of large government programs or the loss of or disruption of revenues on a single contract may reduce our revenues and profits. Such revenue losses could also erode profits on our remaining programs that would have to absorb a larger portion of the fixed corporate costs previously allocated to the expiring programs or discontinued contract work. Our USPS managed inventory program (“MIP”) and our foreign military sales program with the U.S. Navy (“FMS Program”) each constitute a material portion of our revenues. This concentration of our revenue subjects us to risk of material adverse revenue disruptions if customer operational decisions, government contractual, or other issues prevent or delay the fulfillment of work requirements associated with these key programs. In recent years, revenue levels for our FMS Program have fluctuated widely enough to cause material changes in our overall revenue levels and affect our profit margins.

Global economic conditions and political factors could adversely affect our revenues.

Revenues from our government programs for which work is performed in foreign countries are subject to economic conditions in these countries and to political risks posed by ongoing foreign conflicts and potential terrorist activity. Services performed by our employees on our FMS Program are, to a certain extent, dependent on our placement of employees in a client country. Significant domestic and political unrest in client countries can constrain our ability to maintain consistent staffing levels, resulting in a fluctuating level of services performed by our employees. We cannot predict when these conditions will occur or the effect it will have on our FMS Program revenues. Regime changes in these countries can result in government restrictions upon the continuation of ongoing work.

Economic conditions in both the United States and foreign countries, and global prices and availability of oil and other commodities could potentially have an adverse effect on the demand for some of our services, including our aviation services.

Due to the nature of our work we could potentially be exposed to legal actions arising from our operations.

Our work includes many manual tasks, including warehousing, shipping and packing of truck parts inventory, maintaining and repairing military and non-military vehicles and equipment, and maintaining and overhauling U.S. Navy ships. We also repair engines and engine accessories for general aviation jet aircraft. Some of our work efforts involve the handling of hazardous materials. These services may pose certain challenges that could cause us to be exposed to legal and other liabilities arising from performance issues, work related incidents, or employee misconduct that result in damages, injury or death to third parties. Such events could cause us to suffer financial losses and adversely affect our financial condition. (See Item 3. "Legal Proceedings.”)

Technology security and cyber attack risks could potentially impact our financial results.

We face the threat to our computer systems of unauthorized access, computer hackers, computer viruses, malicious code, organized cyber-attacks and other security problems and system disruptions, including possible unauthorized access to our and our clients' proprietary or classified information.

Some of our contract work includes data management and technology services associated with Social Security Administration and military medical and health records. This exposes us to certain information and technology security risks. If there is a security breach of sensitive data in our custody or for which we provide services, we could possibly be held liable for damages to third parties related to such security breach and incur costs to prevent future incidents. We also provide refurbishment, maintenance and training services support to international clients directly and through DoD. Foreign nations with interests that conflict with the international clients we support could be motivated to conduct a cyber-attack to access information on these programs.

Costs associated with preventing or remediating information management security breaches have not had a material adverse effect on our capital expenditures, earnings, or competitive position. However, the occurrence of a future security breach event could potentially have such an adverse effect.

Acquisitions, which have been a part of our business strategy in recent years, present certain risks.

The acquisition of a business that subsequently does not meet expected operating and financial performance targets, the ineffective integration of an acquisition, or our inability to service debt associated with making an acquisition could adversely affect our financial performance. Also, the failure to make or timely complete an acquisition could adversely affect our financial performance.

The nature of our operations and work performed by our employees present certain challenges related to work force management.

Our financial performance is heavily dependent on the abilities of our operating and administrative staff with respect to technical skills, operating performance, pricing, cost management, safety, and administrative and compliance efforts. A wide diversity of contract types, nature of work, work locations, and legal and regulatory complexities challenges our administrative staff and skill sets. We also face challenges associated with our quality of workforce, quality of work, safety, and labor relations compliance. Our current and projected work in foreign countries exposes us to challenges associated with export and ethics compliance, local laws and customs, workforce issues, extended supply chain, political unrest and war zone threats. Failure to attract or retain an adequately skilled workforce, lack of knowledge or training in critical functions, or inadequate staffing levels can result in lost work, reduced profit margins, losses from cost overruns, performance deficiencies, workplace accidents, and regulatory noncompliance.

Our business could be adversely affected by incidents that could cause an interruption in our operations or impose a significant financial liability on us.

Disruption of our operations due to internal or external system or service failures, accidents or incidents involving employees or third parties working in high-risk locations, or natural disasters or other crises could adversely affect our financial performance and condition. A fire, flood, earthquake, or other natural disaster at physical facilities that support key revenue generating operations, or a procurement system or contractual delay could potentially interrupt the revenues from our operations.

We are subject to numerous government rules and regulations that could expose us to potential liabilities or work loss.

We must comply with and are affected by laws and regulations relating to the award, administration and performance of government contracts. A violation of laws or regulations could result in the imposition of fines and penalties or the termination of contracts or debarment from working or bidding on government contracts.

In some instances, these government contract laws and regulations impose terms or rights that are significantly more favorable to the government than those typically available to commercial parties in negotiated transactions. For example, the government may terminate any government contract or subcontract at its convenience, as well as for performance default.

A termination for default could expose us to liability and have a material adverse effect on our ability to compete for future contracts and orders. A termination for default could also impact our past performance and ability to obtain new or additional work. In addition, the government could terminate a prime contract under which we are a subcontractor, irrespective of the quality of services provided by us as a subcontractor.

Additionally, our contract work that is performed by our subcontractors is subject to government compliance, performance requirements and financial risks. If any of our subcontractors fail to timely meet their contractual obligations or have regulatory compliance or other problems, our ability to fulfill our obligations as a prime contractor may be jeopardized.

The aviation industry is highly regulated by the U.S. Federal Aviation Administration ("FAA") and equivalent regulatory agencies in other countries. Aviation engines and engine components that we sell must meet certain airworthiness standards established by the FAA or the equivalent agencies in certain other countries. We also operate repair facilities that are licensed by the FAA and equivalent agencies of certain other countries to perform such services. New and more stringent regulations may be adopted in the future that could have an adverse effect on us.

Our business could be adversely affected by government audits or investigations.

Government agencies, including the Defense Contract Audit Agency and the Department of Labor, routinely audit and investigate government contractors. These agencies review a contractor’s performance under its contracts, cost structure and compliance with applicable laws, regulations and standards. The government also may review the adequacy of, and a contractor’s compliance with, its internal control systems and policies, including the contractor’s purchasing, property, estimating, compensation and management information systems. Any costs found to be improperly allocated to a specific contract will not be reimbursed and any such costs already reimbursed must be refunded. If an audit uncovers improper or illegal activities, we may be subject to civil and criminal penalties and administrative sanctions, including termination of contracts, forfeiture of profits, suspension of payments, fines and suspension or debarment from doing business with the government. In addition, we could suffer serious harm to our reputation if allegations of impropriety were made. As we perform more international work, the risk of compliance with the Foreign Corrupt Practices Act and Export Control Act increases.

Investments in facilities could cause losses if certain work is disrupted or discontinued.

We have made investments in facilities and lease commitments to support specific business programs, work requirements, and service offerings. A slowing or disruption of these business programs, work requirements, or service offerings that results in operating below intended levels could cause us to suffer financial losses.

Environmental and pollution risks could potentially impact our financial results.

Some of our contract work includes the use of chemical solvents and the handling of hazardous materials to maintain, repair, and refurbish vehicles, aircraft engines, and equipment. This exposes us to certain environmental and pollution risks. Costs associated with compliance with Federal, State and local provisions regulating the discharge of materials or that otherwise relate to the protection of the environment have not had a material adverse effect on our capital expenditures, earnings, or competitive position. However, we cannot predict the likelihood of such a material adverse effect should we experience the occurrence of a future environmental or pollution event.

ITEM 1B. Unresolved Staff Comments

None.

ITEM 2. Properties

Our executive and administrative headquarters are located in a five-story building in Alexandria, Virginia, with approximately 95,000 square feet of office space leased by us through April 2027.

We own facilities located in an industrial park in Somerset, Pennsylvania that we use to conduct the operations of our Supply Chain Management Group. These properties consist of approximately 30 acres of land and buildings totaling approximately 239,000 square feet of office, engineering, and warehouse space.

We own two properties that we use to conduct the operations of our Aviation Group. We own and operate a property consisting of approximately one acre of land and a building with approximately 14,000 square feet of warehouse and office space in Miami, Florida. We own and operate a property consisting of a building with approximately 30,500 square feet of warehouse and office space in Independence, Kansas that is located on leased municipal airport land.

We own and operate two facilities in Ladysmith, Virginia. One of these properties consists of approximately 44 acres of land and multiple storage and vehicle maintenance buildings totaling approximately 56,000 square feet of space. The other property consists of 30 acres of land and buildings totaling approximately 13,500 square feet of space. We also own and operate two properties in Texarkana, Arkansas consisting of an aggregate of approximately 16 acres of land and buildings totaling approximately 114,000 square feet. We use these properties primarily to provide refurbishment services for military equipment, storage and maintenance.

We also provide services and products from facilities generally occupied under short-term leases primarily located near customer sites to facilitate communications and enhance program performance. As of December 31, 2016, we leased approximately 24 such facilities with a total of approximately 348,000 square feet of office and warehouse space. Our employees often provide services at customer facilities, limiting our requirement for additional space. We also provide services from locations outside of the United States, generally at foreign shipyards or U.S. military installations.

ITEM 3. Legal Proceedings

Anchorage Litigation and Related Proceedings

In March 2013, a lawsuit, Anchorage vs. Integrated Concepts and Research Corporation, et al., was filed in the Superior Court for the State of Alaska at Anchorage by the Municipality of Anchorage, Alaska (“MOA”) against our subsidiary Integrated Concepts and Research Corporation (“ICRC”) and two former subcontractors of ICRC (the “Anchorage Lawsuit”). The Anchorage Lawsuit asserted breach of contract, professional negligence and negligence in respect of services ICRC performed under its Port of Anchorage Intermodal Expansion Contract with the United States Maritime Administration. ICRC’s contract with the Maritime Administration expired in May 2012. In April 2013, the Anchorage Lawsuit was removed to the United States District Court for the District of Alaska.

In August 2015, a lawsuit, The Charter Oak Fire Insurance Company, The Travelers Indemnity Company of Connecticut and Travelers Property Casualty Company of America vs. Integrated Concepts and Research Corporation, VSE Corporation and Municipality of Anchorage, was filed against VSE and ICRC in the United States District Court for the District of Alaska (the “Coverage Lawsuit”). The plaintiff insurance companies were seeking (a) a declaration by the court that there was no defense or indemnity coverage available to ICRC and VSE for the Anchorage Lawsuit under the insurance policies issued by the plaintiffs and (b) reimbursement of legal fees and costs incurred by the plaintiffs in the defense of uncovered claims in respect of the Anchorage Lawsuit.

On or about January 25, 2017, ICRC, our insurers and MOA fully settled the Anchorage Lawsuit and Coverage Lawsuit. Pursuant to the settlements, ICRC and VSE were released from pending claims in the Anchorage Lawsuit and Coverage Lawsuit and ICRC and our insurers paid MOA approximately $3.8 million, of which $3.0 million was provided by our insurers. The United States District Court approved these lawsuit settlements in February 2017 and dismissed both lawsuits. See our discussion under "Results of Operations" in Part II, Item 7 below for a discussion of the financial effect of these settlements.

On or about September 9, 2016, ICRC filed a claim with the Civilian Board of Contract Appeals (“Board”) against the Maritime Administration for payment of contract closeout costs that were incurred by ICRC in respect of two Port of Anchorage Intermodal Expansion Contracts (the “Contracts”), and legal costs related to the Anchorage Lawsuit. On January 6, 2017, ICRC and the Maritime Administration agreed to a settlement, which the Board approved. Pursuant to the settlement, the U.S. Government paid ICRC $10.4 million in February 2017 in full satisfaction of the contract closeout costs, including interest and any legal costs

or damages arising out of ICRC’s work under the Contracts and the Anchorage Lawsuit. See our discussion under "Results of Operations" in Part II, Item 7 below for a discussion of the financial effect of this settlement.

Heritage Disposal Litigation

In February 2015, a lawsuit, Heritage Disposal & Storage, L.L.C. vs. VSE Corporation, was filed against VSE in the United States District Court for the District of Nebraska (the "Heritage Litigation"). On November 9, 2015, the Heritage Litigation was removed to the United States District Court for the Eastern District of Virginia. The complaint asserted that VSE had not fully paid Heritage for firework storage services rendered by Heritage during the period of October 2010 through August 2015 as a subcontractor under VSE's contract with the U.S. Bureau of Alcohol, Tobacco, Firearms and Explosives for the storage of fireworks seized by the Government. In June 2016, the jury in the Heritage Litigation awarded Heritage damages of approximately $4.8 million, exclusive of interest to be determined by the Court. On January 24, 2017, the United States District Court reduced the jury's award against VSE to approximately $3.5 million and denied Heritage’s request for prejudgment interest. On February 10, 2017, VSE and Heritage entered into an agreement in respect of the Heritage Litigation pursuant to which VSE paid approximately $3.3 million to Heritage in full settlement of the lawsuit.

During the course of the Heritage Litigation, VSE obtained evidence that invoices provided by Heritage under our predecessor contract with the U.S. Department of Treasury (the "Treasury Department") were possibly based on Heritage's improper inflation of the weight of certain seized fireworks stored by Heritage. We filed a voluntary disclosure of this matter with the Inspector General of the Treasury Department in June 2016. We estimated that the possible overbilling of the Government based on Heritage's improper inflation of the weight of seized fireworks stored by Heritage may be approximately $1.5 million. As a result of the United States District Court’s determination in the Heritage Litigation that the jury rejected that Heritage was engaged in a fraudulent billing scheme and that the Government was involved with the original weight estimates, we have determined that VSE did not overbill the Government. In February 2017 we notified the Government that we believe the voluntary disclosure matter is closed, but that we will continue to cooperate with the Government if it decides to continue investigating this matter.

Hawaii Litigation

In May 2012, four complaints were filed in the Circuit Court of the First Circuit, State of Hawaii, by the estates of five deceased individuals and certain of their relatives against VSE and certain other entities and individuals for unspecified damages. The complaints allege, among other things, that the explosion of fireworks and diesel fuel that injured and killed the five individuals in April 2011 was caused by negligence, actions and omissions of VSE and the other defendants and their employees, agents and representatives. The five deceased plaintiffs were employees of Donaldson Enterprises, Inc., which was a vendor retained by VSE to store and dispose of fireworks and other explosives seized by the federal government from entities and individuals illegally in possession of the fireworks and other explosives. VSE had a prime contract with the Treasury Department to support the management and disposal of seized assets, including fireworks and other explosives. VSE has denied the allegations and, together with its insurance carriers, will aggressively defend the proceedings, which are expected to proceed to trial in October 2017. While the results of legal proceedings cannot be predicted with certainty, we do not anticipate that this lawsuit will have a material adverse effect on our results of operations, financial condition, or cash flows.

Aviation Litigation

On or about November 30, 2016, a lawsuit, Arrieta et al. vs. Prime Turbines LLC et al., was filed in the District Court of Texas in Dallas County, by Edgar Arrieta, and four other plaintiffs against VSE's subsidiaries, Kansas Aviation of Independence, LLC (“Kansas Aviation”) and Prime Turbines LLC (“Prime”) and three other unrelated defendants. The other named defendants are Pratt & Whitney of Canada Corporation, Cessna Aircraft Company and Woodward Inc. The Plaintiffs allege that on April 1, 2016, a plane crashed in Mexico, resulting in the death of one plaintiff and serious injuries to two other plaintiffs. Plaintiffs allege that Kansas Aviation and Prime were negligent in providing maintenance, service and inspection of the airplane engine and/or component parts prior to the crash. Plaintiffs state they are seeking monetary relief over $1.0 million from the defendants. Trial is scheduled for May 2018. We have denied the allegations and, together with our insurance carrier, will aggressively defend the proceedings. While the results of legal proceedings cannot be predicted with certainty, we do not anticipate that this lawsuit will have a material adverse effect on our results of operation, financial condition, or cash flows.

In addition to the above-referenced legal proceedings, we may have certain claims in the normal course of business, including legal proceedings, against us and against other parties. In our opinion, the resolution of these other claims will not have a material adverse effect on our results of operations, financial position, or cash flows. However, the results of any legal proceedings cannot be predicted with certainty, therefore, the amount of loss, if any, cannot be reasonably estimated.

Further, from time-to-time, government agencies investigate whether our operations are being conducted in accordance with applicable contractual and regulatory requirements. Government investigations of us, whether relating to government contracts or conducted for other reasons, could result in administrative, civil or criminal liabilities, including repayments, fines or penalties being imposed upon us, or could lead to suspension or debarment from future government contracting. Government investigations often take years to complete and many result in no adverse action against us. We believe, based upon current information, that the outcome of any such government disputes and investigations will not have a material adverse effect on our results of operations, financial position, or cash flows.

ITEM 4. Mine Safety Disclosures

Not applicable.

ITEM 4(a). Executive Officers of Registrant

Our executive officers are listed below, as well as information concerning their age and positions held with VSE. There is no family relationships among any of our executive officers. The executive officers are appointed annually to serve until the first meeting of VSE's Board of Directors (the "Board") following the next annual meeting of stockholders and until their successors are elected and have qualified, or until death, resignation or removal, whichever is sooner.

|

| | | | |

Name | | Age | | Position with Registrant |

Joseph R. Brown | | 60 | | President, Federal Services Group |

Maurice A. Gauthier | | 69 | | Director, Chief Executive Officer, President and Chief Operating Officer |

Paul W. Goffredi | | 59 | | President, VSE's subsidiary VSE Aviation, Inc. |

Thomas M. Kiernan | | 49 | | Vice President, General Counsel and Secretary |

Thomas R. Loftus | | 61 | | Executive Vice President and Chief Financial Officer |

Nancy Margolis | | 61 | | President, VSE's subsidiary Energetics Incorporated and Akimeka LLC |

Chad Wheeler | | 42 | | President, VSE's subsidiary Wheeler Bros., Inc. |

Mr. Brown was appointed the President of the Federal Services Group in May 2015. Our Federal Services Group includes VSE's Global Maritime Services and Global Land Services divisions. Mr. Brown brings over 20 years of experience as a program and business unit manager at VSE. Mr. Brown leads a team whose primary focus is refurbishment services to extend and enhance the life of existing vehicles and equipment, fleet-wide ship and aircraft support, aircraft sustainment and maintenance, foreign military sales and other technical, management, engineering, logistics, maintenance, configuration management, prototyping, technology, and field support services to the U.S. Navy and Marine Corps, U.S. Army and Army Reserve, U.S. Air Force, and other U.S. and foreign military customers. Prior to joining VSE in 1996, Mr. Brown served 20 years active duty in the U.S. Navy. He earned a Bachelor of Business Administration from University of Maryland University College and an Associate of Science in Mechanical Engineering from the University of Tennessee at Knoxville.

Mr. Gauthier has served as VSE's Chief Executive Officer, President and Chief Operating Officer since April 2008, and has served as a Board member since February 2009.

Mr. Goffredi has served as President and Chief Operating Officer of our subsidiary VSE Aviation, Inc. since January 2015, when VSE Aviation, Inc. acquired Prime Turbines LLC (including both U.S. and Germany-based operations), CT Aerospace LLC, Kansas Aviation of Independence, L.L.C. and Air Parts & Supply Co. (collectively, "the Aviation Acquisition"). His focus and background includes business development, strategic OEM and major customer relations, supply chain management, engine and material acquisition, and operational excellence and improvement. Prior to joining VSE, Mr. Goffredi served for three years as Chief Operating Officer for Killick Aerospace, and 13 years with BBA Aviation as Program Director for all Honeywell Engine Programs. Mr. Goffredi received a degree in Business Administration from Mesa State College (Colorado) and holds an MBA in Marketing and Finance from The University of St. Thomas (Texas).

Mr. Kiernan has served as VSE's Vice President, General Counsel and Secretary since November 2008.

Mr. Loftus has served as VSE's Chief Financial Officer and Executive Vice President since March 2002. Mr. Loftus has served in various roles of increasing responsibility at VSE since 1978, and served as VSE's Comptroller, Senior Vice President and Corporate Tax Director from March 1999 to February 2002.

Ms. Margolis has served as the President of Energetics Incorporated since May 2013. She previously served as the Vice President of the Energetics Science and Technology Division from October 1984 to May 2013.

Mr. Wheeler has served as President and Chief Operating Officer of Wheeler Bros., Inc. ("WBI") since July 2013. Since 1991, Mr. Wheeler has served in various roles at WBI, including Senior Vice President of Operations, Senior Vice President of Sales and Marketing, and Marketing and Sales Manager. While serving as Marketing and Sales Manager, Mr. Wheeler coordinated implementation of WBI's Managed Inventory Program which is used at the USPS' Vehicle Maintenance Facilities throughout the country. Mr. Wheeler graduated summa cum laude from Indiana University of Pennsylvania in 1998 with a degree in Marketing.

PART II

ITEM 5. Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

(a)Market Information

VSE common stock, par value $0.05 per share, is traded on The NASDAQ Global Select Market, trading symbol, "VSEC," Newspaper listing, "VSE."

In May 2016, our Board approved a two-for-one stock split effected in the form of a stock dividend ("Stock Split"). The Stock Split had a record date of July 20, 2016 and stock distribution occurred on August 3, 2016. All share and per share amounts have been adjusted to give retroactive effect to the increased number of shares of common stock outstanding due to the Stock Split.

The following table sets forth the range of high and low sales price (based on information reported by The NASDAQ Global Select Market) and cash dividend per share information for our common stock for each quarter and annually during the last two years. Sales prices and cash dividend per share information have been adjusted for the Stock Split.

|

| | | | | | | | | | | | |

Quarter Ended | | High | | Low | | Dividends |

2015: | | | | | | |

March 31 | | $ | 42.03 |

| | $ | 31.50 |

| | $ | 0.050 |

|

June 30 | | 41.95 |

| | 26.16 |

| | 0.055 |

|

September 30 | | 27.68 |

| | 16.76 |

| | 0.055 |

|

December 31 | | 33.93 |

| | 19.04 |

| | 0.055 |

|

For the Year | | $ | 42.03 |

| | $ | 16.76 |

| | $ | 0.215 |

|

| | | | | | |

2016: | | |

| | |

| | |

|

March 31 | | $ | 35.60 |

| | $ | 26.38 |

| | $ | 0.055 |

|

June 30 | | 35.98 |

| | 30.86 |

| | 0.060 |

|

September 30 | | 38.23 |

| | 29.94 |

| | 0.060 |

|

December 31 | | 42.69 |

| | 26.16 |

| | 0.060 |

|

For the Year | | $ | 42.69 |

| | $ | 26.16 |

| | $ | 0.235 |

|

(b)Holders

As of February 1, 2017, VSE common stock, par value $0.05 per share, was held by approximately 227 stockholders of record. The number of stockholders of record is not representative of the number of beneficial holders because many of VSE's shares are held by depositories, brokers or nominees.

(c)Dividends

In 2015 cash dividends were declared quarterly at the annual rate of $0.20 per share through March 31, 2015, and at the annual rate of $0.22 per share commencing June 1, 2015.

In 2016 cash dividends were declared quarterly at the annual rate of $0.22 per share through March 31, 2016, and at the annual rate of $0.24 per share commencing June 1, 2016.

Pursuant to our bank loan agreement (see Note 7, Debt, of "Notes to Consolidated Financial Statements" in Item 8 of this Form 10-K), the payment of cash dividends is subject to annual rate restrictions. We have paid cash dividends each year since 1973 and have increased our dividend each year since 2004.

(d)Certain Sales and Repurchases of VSE Common Stock

During the fiscal year covered by this Form 10-K, VSE did not sell any of its equity securities that were not registered under the Securities Act of 1933, as amended. During the fourth quarter of the fiscal year covered by this Form 10-K, no purchases of equity securities of VSE were made by or on behalf of VSE or any "affiliated purchaser" (as defined in Exchange Act Rule 10b-18 (a)(3)) other than 15,636 shares of our restricted common stock that were voluntarily forfeited to VSE by participants in its 2006 Restricted Stock Plan to cover their personal tax liability for restricted stock awards.

(e)Equity Compensation Plan Information

We have two compensation plans approved by our stockholders under which our equity securities are authorized for issuance to employees and directors: (i) the VSE Corporation 2004 Non-Employee Directors Stock Plan and (ii) the VSE Corporation 2006 Restricted Stock Plan.

As of December 31, 2016, 132,569 shares of VSE common stock were available for future issuance under the VSE Corporation 2004 Non-Employee Directors Stock Plan and 476,140 shares of VSE common stock were available for future issuance under the VSE Corporation 2006 Restricted Stock Plan.

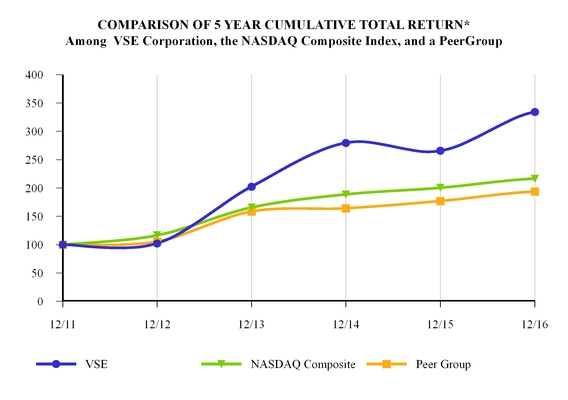

Performance Graph

Set forth below is a line graph comparing the cumulative total return of VSE common stock with (a) a performance index for the broad market (The NASDAQ Global Select Market) on which VSE common stock is traded and (b) a published industry index. VSE common stock is traded on The NASDAQ Global Select Market, and our industry group is engineering and technical services (formerly SIC Code 8711). Accordingly, the performance graph compares the cumulative total return for VSE common stock with (a) an index for The NASDAQ Global Select Market (U.S. companies) ("NASDAQ Index") and (b) our peer group.

*$100 invested on 12/31/11 in stock or index, including reinvestment of dividends.

Fiscal year ending December 31.

Performance Graph Table

|

| | | | | | | | | | | |

| 2011 | | 2012 | | 2013 | | 2014 | | 2015 | | 2016 |

VSE | 100 | | 102.24 | | 202.28 | | 279.52 | | 265.58 | | 334.15 |

NASDAQ Composite | 100 | | 116.41 | | 165.47 | | 188.69 | | 200.32 | | 216.54 |

Peer Group | 100 | | 105.54 | | 158.42 | | 164.29 | | 177.03 | | 193.76 |

ITEM 6. Selected Financial Data

(in thousands, except per share data)

|

| | | | | | | | | | | | | | | | | | | |

| Years ended December 31, |

| 2016 | | 2015 | | 2014 | | 2013 | | 2012 |

| | | | | | | | | |

Revenues | $ | 691,790 |

| | $ | 533,982 |

| | $ | 424,071 |

| | $ | 471,638 |

| | $ | 546,755 |

|

| | | | | | | | | |

Income from continuing operations | $ | 26,793 |

| | $ | 24,918 |

| | $ | 20,489 |

| | $ | 23,990 |

| | $ | 27,364 |

|

Loss from discontinued operations | — |

| | — |

| | (1,124 | ) | | (1,138 | ) | | (6,070 | ) |

Net income | $ | 26,793 |

| | $ | 24,918 |

| | $ | 19,365 |

| | $ | 22,852 |

| | $ | 21,294 |

|

| | | | | | | | | |

Basic earnings per share: | | | | | | | | | |

Income from continuing operations | $ | 2.48 |

| | $ | 2.32 |

| | $ | 1.91 |

| | $ | 2.25 |

| | $ | 2.59 |

|

Loss from discontinued operations | — |

| | — |

| | (0.10 | ) | | (0.11 | ) | | (0.58 | ) |

Net income | $ | 2.48 |

| | $ | 2.32 |

| | $ | 1.81 |

| | $ | 2.14 |

| | $ | 2.01 |

|

| | | | | | | | | |

Diluted earnings per share: | | | | | | | | | |

Income from continuing operations | $ | 2.47 |

| | $ | 2.31 |

| | $ | 1.91 |

| | $ | 2.25 |

| | $ | 2.58 |

|

Loss from discontinued operations | — |

| | — |

| | (0.10 | ) | | (0.11 | ) | | (0.57 | ) |

Net income | $ | 2.47 |

| | $ | 2.31 |

| | $ | 1.81 |

| | $ | 2.14 |

| | $ | 2.01 |

|

| | | | | | | | | |

Cash dividends per common share | $ | 0.235 |

| | $ | 0.215 |

| | $ | 0.195 |

| | $ | 0.175 |

| | $ | 0.155 |

|

|

| | | | | | | | | | | | | | | | | | | |

| As of December 31, |

| 2016 | | 2015 | | 2014 | | 2013 | | 2012 |

| | | | | | | | | |

Working capital | $ | 110,021 |

| | $ | 100,780 |

| | $ | 33,037 |

| | $ | 46,828 |

| | $ | 64,209 |

|

| | | | | | | | | |

Total assets | $ | 661,839 |

| | $ | 617,354 |

| | $ | 353,430 |

| | $ | 380,077 |

| | $ | 409,572 |

|

| | | | | | | | | |

Long-term debt | $ | 193,621 |

| | $ | 215,243 |

| | $ | 23,483 |

| | $ | 64,221 |

| | $ | 115,924 |

|

| | | | | | | | | |

Long-term lease obligations | $ | 21,959 |

| | $ | 23,251 |

| | $ | 24,584 |

| | $ | 25,721 |

| | $ | 27,435 |

|

| | | | | | | | | |

Stockholders' equity | $ | 255,194 |

| | $ | 229,309 |

| | $ | 205,489 |

| | $ | 186,803 |

| | $ | 164,335 |

|

This consolidated summary of selected financial data should be read in conjunction with Management's Discussion and Analysis of the Financial Condition and Results of Operations included in Item 7 of this Form 10-K and with the Consolidated Financial Statements and related Notes included in Item 8 of this Form 10-K. The historical results set forth in this Item 6 are not necessarily indicative of the results of operations to be expected in the future.

ITEM 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

Executive Overview

Customers and Services

We are a diversified services and supply chain management company that assists our clients in sustaining, extending the service life, and improving the performance of their transportation, equipment, and other assets and systems. We provide logistics and distribution services for legacy systems and equipment and professional and technical services to the United States Government (the "government"), including the United States Department of Defense ("DoD"), the United States Postal Service ("USPS"), federal civilian agencies, and to commercial and other customers. Our largest customers are the DoD and the USPS. Our operations include supply chain management solutions, parts supply and distribution, and maintenance, repair, and overhaul (“MRO”) services for vehicle fleet, aviation, and other clients; vehicle and equipment maintenance and refurbishment; logistics; engineering; energy and environmental services; IT and health care IT solutions; and consulting services. See Item 1 “Business - Revenues and Contracts” above for revenues by customer.

Organization and Segments

Our operations are conducted within four reportable segments aligned with our management groups: 1) Supply Chain Management; 2) Aviation; 3) Federal Services; and 4) IT, Energy and Management Consulting. Beginning in 2017, we are consolidating our Federal Services Group and IT, Energy and Management Consulting Group into a single management group and reportable segment.

Supply Chain Management Group - Our Supply Chain Management Group provides sourcing, acquisition, scheduling, transportation, shipping, logistics, data management, and other services to assist our clients with supply chain management efforts. This group consists of our subsidiaries Wheeler Bros., Inc. ("WBI") and Ultra Seating Company. The primary revenue source for this group is WBI's USPS Managed Inventory Program ("MIP") that supplies vehicle parts and mission critical supply chain support for the USPS truck fleet. Other current work efforts include managed inventory services and parts sales to support commercial client truck fleets, parts sales to DoD, and other projects to support the USPS.

Aviation Group - Our Aviation Group provides MRO services, parts supply and distribution, and supply chain solutions for general aviation jet aircraft engines and engine accessories. This group consists of VSE Aviation, Inc. and the four aviation businesses we acquired in January 2015. These businesses have a diversified client base serving corporate and private aircraft owners, regional airlines, aviation manufacturers, other aviation MRO providers, cargo transporters, and agricultural clients.

Federal Services Group - Our Federal Services Group provides foreign military sales services, refurbishment services to extend and enhance the life of existing vehicles and equipment, fleet-wide ship and aircraft support, aircraft sustainment and maintenance, and other technical, management, engineering, logistics, maintenance, configuration management, prototyping, technology, and field support services to the U.S. Navy and Marine Corps, U.S. Army and Army Reserve, U.S. Air Force, and other customers. Significant work efforts for this group include assistance to the U.S. Navy in executing its Foreign Military Sales (“FMS”) Program for surface ships sold, leased or granted to foreign countries, our Red River Army Depot Equipment Related Services Program (“RRAD ERS”) providing on-site logistics support for Red River Army Depot at Texarkana, Texas, our Fort Benning Logistics Support Services Program supporting base operations and logistics at Fort Benning, Georgia, and various vehicle and equipment refurbishment, maintenance and sustainment programs for U.S. Army commands.

IT, Energy and Management Consulting Group - Our IT, Energy and Management Consulting Group provides technical and consulting services primarily to various DoD and federal civilian agencies, including the United States Departments of Energy, Homeland Security, and Interior; the Social Security Administration; the National Institutes of Health; customers in the military health system; and other government agencies and commercial clients. This group consists of our subsidiaries Energetics Incorporated ("Energetics") and Akimeka, LLC ("Akimeka"). Energetics provides technical, policy, business, and management support in areas of energy modernization, clean and efficient energy, climate change mitigation, infrastructure protection, and measurement technology. Akimeka offers solutions in fields that include medical logistics, medical command and control, e-health, information assurance, public safety, enterprise architecture development, business continuity, program and portfolio management, network IT services, cloud managed services, systems design and integration, quality assurance services, and product and process improvement services.

Concentration of Revenues

|

| | | | | | | | | | | | | | | | | | |

|

| (in thousands) Years ended December 31, |

Source of Revenues | | 2016 | | % | | 2015 | | % | | 2014 | | % |

USPS | | $ | 181,215 |

| | 26 | | $ | 184,876 |

| | 35 | | $ | 167,268 |

| | 40 |

FMS Program | | 169,754 |

| | 25 | | 76,476 |

| | 14 | | 86,399 |

| | 20 |

Other | | 340,821 |

| | 49 | | 272,630 |

| | 51 | | 170,404 |

| | 40 |

Total Revenues | | $ | 691,790 |

| | 100 | | $ | 533,982 |

| | 100 | | $ | 424,071 |

| | 100 |

Management Outlook

We saw steady revenue growth in 2016, as revenue increased on a quarter to quarter basis throughout the year and was up 30% over the prior year. The improvements in our revenue levels were led by renewed vigor in our Federal Services Group markets, for which revenues increased by 83%. Strong contract funding awards in 2016 allowed us to finish the year with a contract funded backlog that positions us well as we head into 2017. Increased revenues from our Supply Chain Management Group and a full year of revenue from our Aviation Group (as compared to eleven months in 2015 when we acquired these businesses) also contributed to our revenue growth in 2016.

We are encouraged to see contributions to our Federal Services Group revenue base from both our long time programs and newer programs. Activity on our FMS Program has increased over the past year, including work to transfer two frigates to Taiwan and equipment supply services to U.S. Navy foreign client countries. Our equipment refurbishment services for U.S. Army Reserve transportation equipment and other assets continue to be a key service offering to this legacy customer. Our newer programs enhancing revenue growth include our RRAD ERS Program, started in May 2016, and our Fort Benning Logistics Support Services Program, started in August 2015. These four programs, including a full year of revenue on our RRAD ERS Program in 2017, as well as additional smaller new work efforts, provide our Federal Services Group with a solid revenue base. Contract funding increases resulted in bookings of $458 million in 2016 and contract funded backlog of $322 million for our federal contracting businesses as of the end 2016, which will help sustain our 2017 federal contracting revenues. Additionally, we have developed strong international business relationships through our decades of work with foreign client countries. We are extending these relationships to market our services to several international clients.

Revenues for our Supply Chain Management Group have increased in 2016 at more modest levels than the previous two years. Although our vehicle parts supply and inventory management support for the USPS delivery vehicle fleet continue to be the primary drivers of this group’s successful results, 2016 revenue growth for this group has been provided by greater diversification and growth of parts sales to the DoD, increased supply chain and inventory management support for commercial vehicle fleets, and revenue from our acquisition of Ultra Seating Company in December 2015. We continue to broaden our base of commercial clients and make progress toward capturing new commercial vehicle fleet clients.

We are a key partner with the USPS and our mission critical supply chain support should continue to be essential in sustaining the aging USPS fleet as this client embarks on a lengthy procurement process to acquire a new class of delivery vehicles to both augment and replace older vehicles. The USPS anticipates the first deployment of a small number of newly produced vehicles will occur in three or four years. At that point in time, production and procurement of vehicles will be scheduled to occur annually over a seven-year period. USPS' previously published vehicle procurement time lines continue to experience changes and delays. Based on the size, scope, and complexity of USPS' new vehicle procurement strategy, we cannot be certain of the timing and quantities of new vehicles to be deployed. We also cannot determine the timing or number of existing delivery vehicles that will be redeployed for other routes or purposes.

While we will not participate in the competition to provide new vehicles, we will be seeking to participate with the selected providers to offer original content, program management, and warranty support. Aftermarket parts supply and supply chain services to support the USPS' newly acquired vehicles will be part of our model in addition to continuing our support for older USPS vehicles that remain in service. In 2016 the USPS disclosed that 1.1 million addresses were added to their delivery network and shipping and packaging volume increased by half a billion items in 2015, all contributing to an increased requirement for delivery capacity which may require a combination of both old and new vehicles for longer than currently planned. While we cannot predict with certainty the impact on our future revenues once the USPS new delivery vehicle procurement begins, we believe that our years of service and knowledge of this client’s needs strategically position us to participate in providing parts supply and supply chain services for newly procured vehicles and to offer total parts availability for existing older vehicles that remain in service.

Our Aviation Group contributed approximately 19% of our revenues and is a significant part of our strategy to expand our markets for sustainment services, while diversifying our customer and revenue base and strengthening growth potential. This group has provided us with a wide range of new clients, competencies and key industry relationships that offer potential synergies as we seek to extend these service offerings to our traditional U.S. and international military client base. Revenue and operating income for this group may experience fluctuations due to market demand and the mix of products sold.

As 2016 ended and 2017 began, we settled several pending litigation matters, as discussed above in Item 3. "Legal Proceedings." In January 2017, we settled the Anchorage Lawsuit, a related insurance coverage lawsuit, and our claim against the U.S. Maritime Administration. These matters were associated with our ICRC subsidiary's contract work with the U.S. Maritime Administration that ended in 2012. These settlements include our release from related claims and the finalization of our contract close-out with the U.S. Maritime Administration which included a payment to ICRC for unreimbursed contract work and certain legal costs. The net benefit to our operating income for the year ended December 31, 2016 resulting primarily from the contract close-out is approximately $1.4 million. Also in February 2017, we settled the Heritage Litigation discussed above in Item 3, which reduced 2016 operating income by approximately $3.3 million.

Bookings and Funded Backlog

Revenues for government contract work performed by our Federal Services and IT, Energy and Management Consulting groups depend on contract funding (“bookings”), and bookings generally occur when contract funding documentation is received. Funded contract backlog is an indicator of potential future revenue for these groups. While bookings and funded contract backlog generally result in revenue, we may occasionally have funded contract backlog that expires or is de-obligated upon contract completion and does not generate revenue.

A summary of our bookings and revenues for our Federal Services and IT, Energy and Management groups for the years ended December 31, 2016, 2015 and 2014, and funded contract backlog for these groups as of December 31, 2016, 2015 and 2014 is as follows (in millions):

|

| | | | | | | | | | | |

| 2016 | | 2015 | | 2014 |

Bookings | $ | 458 |

| | $ | 281 |

| | $ | 217 |

|

Revenues | $ | 353 |

| | $ | 217 |

| | $ | 252 |

|

Funded Backlog | $ | 322 |

| | $ | 238 |

| | $ | 193 |

|

Recently Issued Accounting Pronouncements

For a description of recently announced accounting standards, including the expected dates of adoption and estimated effects, if any, on our consolidated financial statements, see "Recently Issued Accounting Pronouncements" in Note 1 of the Notes to our Consolidated Financial Statements in this Form 10-K.

Critical Accounting Policies

Our consolidated financial statements are prepared in accordance with accounting principles generally accepted in the United States, which require us to make estimates and assumptions. We believe the following critical accounting policies affect the more significant accounts, particularly those that involve judgments, estimates and assumptions used in the preparation of our consolidated financial statements.

Revenue Recognition

Revenue is recognized when persuasive evidence of an arrangement exists, delivery has occurred or services have been rendered, the fee is fixed or determinable, and collection is probable.

Substantially all of our Supply Chain Management Group revenues result from the sale of vehicle parts to clients. We recognize revenue from the sale of vehicle parts when the customer takes ownership of the parts.

Our Aviation Group revenues are recognized upon the shipment or delivery of products to customers based on when title or risk of loss transfers to the customer. Sales returns and allowances are not significant.

Substantially all of our Federal Services and IT, Energy and Management Consulting work is performed for our customers on a contract basis. The three primary types of contracts used are cost-type, fixed-price and time and materials. Revenues result from work performed on these contracts by our employees and our subcontractors and from costs for materials and other work related costs allowed under our contracts.

Revenues on cost-type contracts are recorded as contract allowable costs are incurred and fees are earned. Our FMS Program contract is a cost plus award fee contract. This contract has terms that specify award fee payments that are determined by performance and level of contract activity. Award fees are made during the year through a contract modification authorizing the award fee that is issued subsequent to the period in which the work is performed. We recognize award fee income on the FMS Program contract when the fees are fixed or determinable. Due to such timing and fluctuations in the level of revenues, profits as a percentage of revenues on this contract will fluctuate from period to period.

Revenue recognition methods on fixed-price contracts will vary depending on the nature of the work and the contract terms. Revenues on fixed-price service contracts are recorded as work is performed, typically ratably over the service period. Revenues on fixed-price contracts that require delivery of specific items are recorded based on a price per unit as units are delivered.

Revenues for time and materials contracts are recorded on the basis of contract allowable labor hours worked multiplied by the contract defined billing rates, plus the direct costs and indirect cost burdens associated with materials and subcontract work used in performance on the contract. Generally, profits on time and materials contracts result from the difference between the cost of services performed and the contract defined billing rates for these services.

A summary of revenues for our operating groups, including a summary by contract type for our Federal Services and IT, Energy and Management Consulting groups, for the years ended December 31 is presented below (in thousands).

|

| | | | | | | | | | | | | | | | | |

Contract Type | 2016 Revenues | | % | | 2015 Revenues | | % | | 2014 Revenues | | % |

Cost-type | $ | 207,047 |

| | 29.9 | | $ | 100,447 |

| | 18.8 | | $ | 120,915 |

| | 28.5 |

Fixed-price | 75,213 |

| | 10.9 | | 74,490 |

| | 13.9 | | 87,807 |

| | 20.7 |

Time and materials | 70,589 |

| | 10.2 | | 42,544 |

| | 8.0 | | 42,867 |

| | 10.1 |

Total Federal Services and IT, Energy and Management Consulting revenues | 352,849 |

| | 51.0 | | 217,481 |

| | 40.7 | | 251,589 |

| | 59.3 |

| | | | | | | | | | | |

Supply Chain Management and Aviation revenues | 338,941 |

| | 49.0 | | 316,501 |

| | 59.3 | | 172,482 |

| | 40.7 |

Total revenues | $ | 691,790 |

| | 100.0 | | $ | 533,982 |

| | 100.0 | | $ | 424,071 |

| | 100.0 |

We will occasionally perform work at risk, which is work performed prior to formalizing contract funding for such work. Revenue related to work performed at risk is not recognized until it can be reliably estimated and its realization is probable. We recognize this “risk funding” as revenue when the associated costs are incurred or the work is performed. We are at risk of loss for any risk funding not received. Revenues recognized as of December 31, 2016 include approximately $2.1 million for which we have not received formalized funding. We believe that we are entitled to reimbursement and expect to receive all of this funding.

Goodwill and Intangible Assets

We have five reporting units, including four reporting units with goodwill. Goodwill is subject to a review for impairment at least annually. We perform an annual review of goodwill for impairment during the fourth quarter and whenever events or changes in circumstances indicate that the carrying value may not be recoverable. The impairment assessment requires us to estimate the fair value of our reporting units and involves the use of subjective assumptions.

We estimated the fair value of our reporting units using a weighting of fair values derived from the income approach, market approach, and comparative transactions approach with the heaviest weighting placed on the income approach. Under the income approach, we calculate the fair value of a reporting unit based on the present value of estimated future cash flows. Cash flow projections are based on our estimates of revenue growth rates and operating margins, taking into consideration industry and market conditions. The discount rate used is based on a weighted average cost of capital adjusted for the relevant risk associated with the characteristics of the business and the projected cash flows.

In the fourth quarter of 2016, we performed our annual goodwill impairment analysis for each of our reporting units with goodwill. The results of the impairment analysis indicated that our reporting units had fair values substantially in excess of their carrying values with the exception of our Akimeka and Aviation reporting units.